ファイル:Lending & Borrowing Decisions - 10 19 08.png

{kind=link}

{kind=link}

{kind=link}

元のファイル (960 × 720 ピクセル、ファイルサイズ: 15キロバイト、MIME タイプ: image/png)

ウィキメディア・コモンズのファイルページにある説明を、以下に表示します。

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

概要

| 解説 |

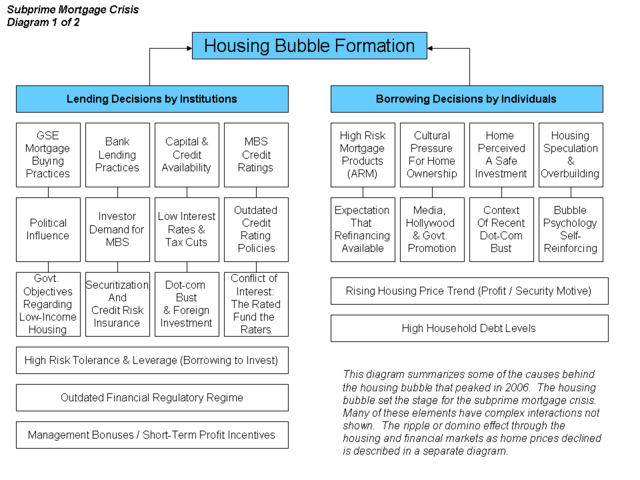

English: Causes of the Housing Bubble OverviewSee the United States housing bubble and subprime mortgage crisis for in-depth discussion and citations. A brief summary of each vertical "string" of causes is included below. While there are many factors that influenced the housing bubble, fundamentally a bubble is built one transaction at a time. Risky lending decisions were made by institutions and risky borrowing decisions were made by both individuals and institutions. According to the Pew Research Center, “There is a broad public consensus regarding the causes of the current problems with financial institutions and markets: 79 percent say people taking on too much debt has contributed a lot to the crisis, while 72 percent say the same about banks making risky loans.”[1] Lending Decisions by Institutions

Borrowing Decisions by Individuals

Transition to the Subprime Mortgage Crisisthumb|A diagram of the elements of the subprime crisis Once housing prices began to fall in June-July 2006, homeowners were often stuck with mortgages they could not afford or refinance. Delinquencies and foreclosures increased dramatically. As mortgage payments fell, the money flowing into MBS decreased during 2007. Many financial institutions suffered enormous losses, with hundreds of mortgage companies and several major financial institutions going bankrupt. Due to uncertainty regarding the financial condition of many financial institutions and banks dramatically increasing lending standards, loanable funds liquidity became less available. This is further described in the second subprime crisis diagram at right. Additional SourcesComprehensive discussions of housing bubbles and the crisis are at: Other Specific contributing causes:

Caveats

SourcesThe letters from Fed Chairman Bernanke provide a helpful explanation of the subject.[4] [5] Further, several cover stories and in-depth articles appeared in the Economist[6] [7] [8] and Business Week.[9] Former Federal Reserve Chairman Greenspan wrote an Op Ed piece for the Wall Street Journal that summarizes the crisis from a variety of angles.[10] Economist Joseph Stiglitz summarized his views on the causes of the crisis.[11] |

| 日付 | |

| 原典 | 投稿者自身による著作物 (Original text: I created this work entirely by myself.) |

| 作者 | Farcaster (talk) 01:39, 20 October 2008 (UTC) |

{kind=link}

- ↑ NY Times-

- ↑ AEI-The Destruction of Fannie & Freddie

- ↑ Shiller-Infectious Exuberance-The Atlantic

- ↑ FRB: Speech-Bernanke, Financial Markets, the Economic Outlook, and Monetary Policy -January 10, 2008

- ↑ FRB: Speech-Bernanke, The Recent Financial Turmoil and its Economic and Policy Consequences-October 15, 2007

- ↑ The credit crunch | Postcards from the ledge | Economist.com]

- ↑ CSI: credit crunch | Economist.com]

- ↑ America's economy | Getting worried downtown | Economist.com]

- ↑ Housing Meltdown

- ↑ The Wall Street Journal Online - Featured Article

- ↑ Stiglitz-Capitalist Fools

ライセンス

- あなたは以下の条件に従う場合に限り、自由に

- 共有 – 本作品を複製、頒布、展示、実演できます。

- 再構成 – 二次的著作物を作成できます。

- あなたの従うべき条件は以下の通りです。

- 表示 – あなたは適切なクレジットを表示し、ライセンスへのリンクを提供し、変更があったらその旨を示さなければなりません。これらは合理的であればどのような方法で行っても構いませんが、許諾者があなたやあなたの利用行為を支持していると示唆するような方法は除きます。

- 継承 – もしあなたがこの作品をリミックスしたり、改変したり、加工した場合には、あなたはあなたの貢献部分を元の作品とこれと同一または互換性があるライセンスの下に頒布しなければなりません。

|

この文書は、フリーソフトウェア財団発行のGNUフリー文書利用許諾書 (GNU Free Documentation License) 1.2またはそれ以降のバージョンの規約に基づき、複製や再配布、改変が許可されます。不可変更部分、表紙、背表紙はありません。このライセンスの複製は、GNUフリー文書利用許諾書という章に含まれています。 |

元のアップロードログ

{kind=link}

- 2008-10-21 02:40 Farcaster 960×720× (15164 bytes)

- 2008-10-20 01:39 Farcaster 960×720× (11732 bytes) {{Information |Description=Causes of the Housing Bubble |Source=I created this work entirely by myself. |Date=10 19 2008 |Author=~~~~ |other_versions= }}

ファイルの履歴

過去の版のファイルを表示するには、その版の日時をクリックしてください。

| 日付と時刻 | サムネイル | 寸法 | 利用者 | コメント | |

|---|---|---|---|---|---|

| 現在の版 | 2010年10月14日 (木) 00:45 | | 960 × 720 (15キロバイト) | Hideokun | {{Information |Description={{en|Causes of the Housing Bubble<br/> ==Overview== See the en:United States housing bubble and en:subprime mortgage crisis for in-depth discussion and citations. A brief summary of each vertical "string" of causes |

ファイルの使用状況

以下の 2 ページがこのファイルを使用しています:

グローバルなファイル使用状況

以下に挙げる他のウィキがこの画像を使っています:

- en.wikipedia.org での使用状況

- hi.wikipedia.org での使用状況

- ta.wikipedia.org での使用状況

{kind=link}

{kind=link}